US Dollar May Fall as SGD, PHP Rise. USD/INR Eyes China-India Tensions

US DOLLAR, SINGAPORE DOLLAR, INDONESIAN RUPIAH, MALAYSIAN RINGGIT, PHILIPPINE PESO – TALKING POINTS

- US Dollar weakened against ASEAN currencies as stocks soared

- USD/SGD, USD/IDR, USD/MYR, USD/PHP outlook biased lower

- China-India border tensions stirring volatility in INR and Nifty 50

US DOLLAR ASEAN WEEKLY RECAP

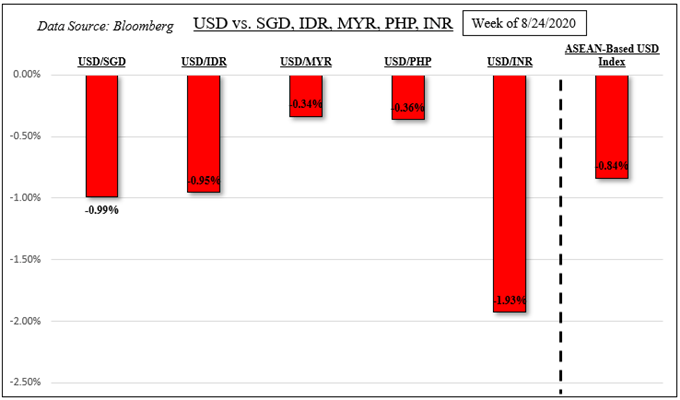

The haven-linked US Dollar extended losses against its ASEAN counterparts this past week. The Singapore Dollar, Indonesian Rupiah, Malaysian Ringgit and Philippine Peso all gained ground. As anticipated, the focus for ASEAN currencies remained on external developments given a relatively light local economic docket. A dovish Federal Reserve seemed to be a key driver that pushed equities higher, denting the USD.

Another notable standout in the emerging market FX space was the Indian Rupee. USD/INR declined almost 2% over the course of one week, the most since December 2018 – see chart below. A combination of capital inflows and the Reserve Bank of India refraining from intervening in foreign exchange markets likely drove the aggressive gains seen in the Indian Rupee.

LAST WEEK’S US DOLLAR PERFORMANCE

EXTERNAL EVENT RISK – ISM MANUFACTURING & SERVICES DATA, NON-FARM PAYROLLS

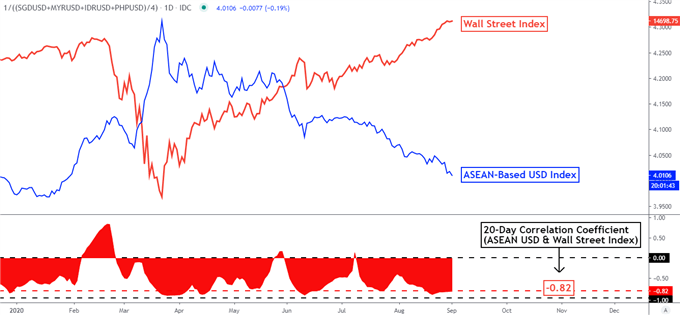

What is interesting to see is that USD/SGD, USD/IDR, USD/PHP and USD/MYR seem to be focusing on fundamental dynamics driving equity valuations in the United States rather than from Emerging Market ones – see next chart below. Investors often look to the world’s largest economy for insight into how global growth can develop.

ISM manufacturing and services data are due on Tuesday and Thursday respectively. On Wednesday durable goods orders will cross the wires. Then, the week will wrap up with arguably the most high-impact event risk, non-farm payrolls (NFPs). The Citi Economic Surprise Index tracking the US continues to remain in elevated positive territory. That suggests economists continue underestimating the health and vigor of the recovery.

However, the gauge just declined to its lowest since early July, perhaps suggesting that expectations are slowly aligning closer towards reality. An environment with diminishing rosy beats in data could perhaps cool the pace of weakness in the US Dollar should stock gains level out. But, the broader trajectory for the Greenback could remain bearish with the Federal Reserve now allowing inflation to temporarily overshoot target.

Of course, volatility risk remains for ASEAN currencies. The VIX ‘fear gauge’ closed at its highest since the middle of July. Should market mood sour and cause capital to flow out of emerging markets, the haven-oriented US Dollar could see swift and brisk appreciation.

ASEAN, SOUTH ASIA EVENT RISK – PHILIPPINE CPI, SINGAPORE RETAIL SALES, CHINA-INDIA TENSIONS

Focusing on ASEAN event risk, the Philippine Peso and Singapore Dollar face local CPI and retail sales data respectively. Earlier this month, the Philippine Central Bank (BSP) paused cutting rates amid rising near term inflation expectations. Higher-than-expected inflation that further pours cold water on BSP easing bets could offer more support to PHP.

Meanwhile, the Indian Rupee and Nifty 50 could be vulnerable to rising China-India geopolitical tensions. Over the weekend, India said that China made provocative military movements along a disputed border in the Himalayan Mountains. The latter disputed the claim saying that its border troops never crossed the line.

In June, similar tensions sent USD/INR higher as the Nifty 50 fell. On Monday, the latter sank 2.23% in the worst 24-hour performance since May. Softer-than-expected Indian second-quarter GDP data may have also played a role. India’s economy shrank 23.9% y/y versus -18.0% expected, the worst among the major nations.

On August 31, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets Index, excluding China, (EMXC) stood at -0.06. This is from -0.33 in the preceding week. Meanwhile, the 20-day rolling correlation between my ASEAN-based US Dollar index and my Wall Street index remains elevated at -0.82 versus -0.88 over the same period. Values closer to -1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-BASED USD INDEX VERSUS WALL STREET INDEX – DAILY CHART

Comments

Post a Comment